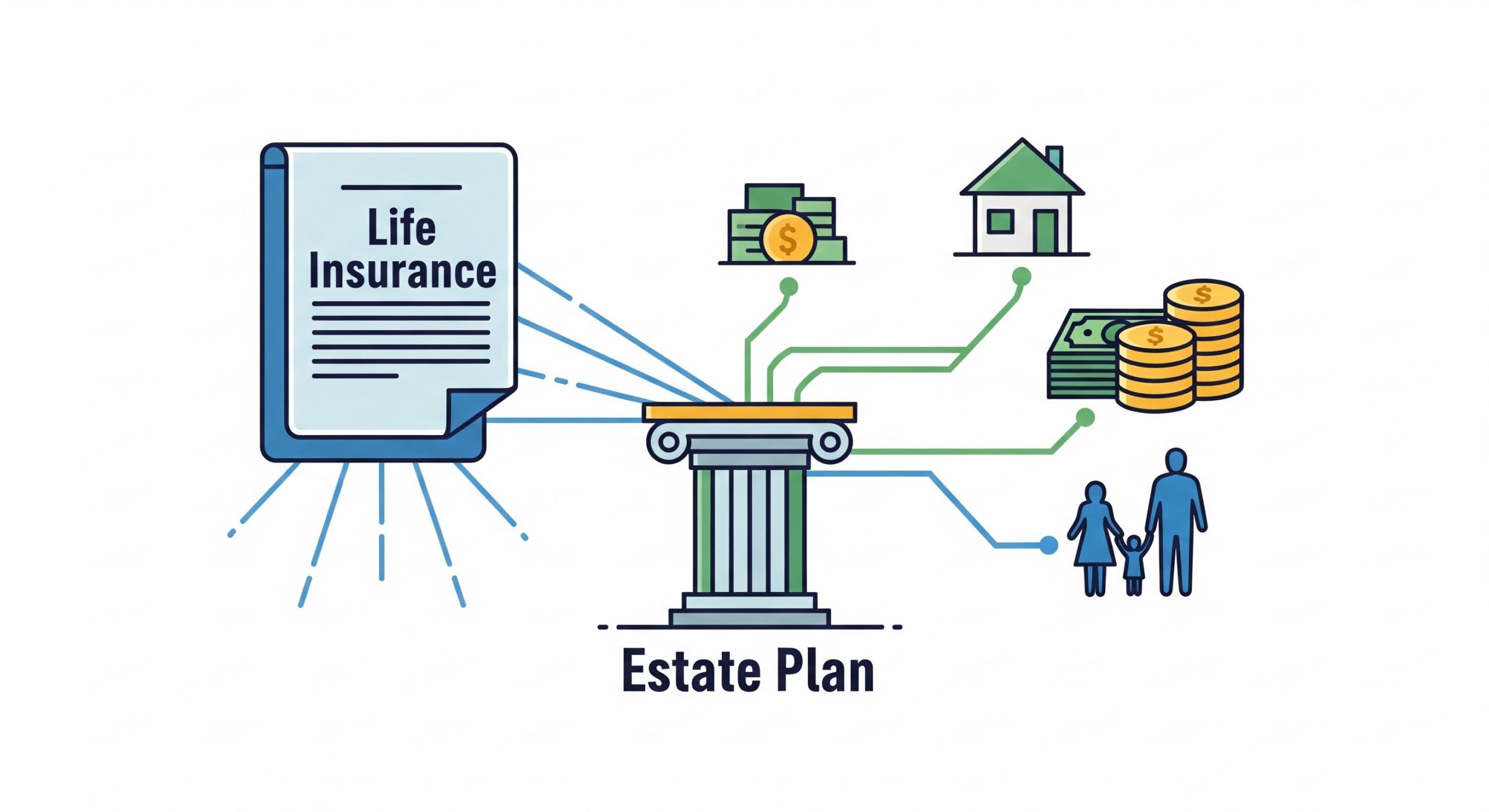

5 Ways Life Insurance Can Support Your Estate Plan

Life insurance isn’t only about income replacement. It can also play a practical role in estate planning by providing liquidity, improving fairness between beneficiaries, and helping your family avoid tough financial decisions during a stressful time.

1) Provides Immediate Cash When It’s Needed Most.

Settling an estate can come with expenses—final costs, outstanding debts, legal fees, and more. Life insurance can create a pool of cash so loved ones don’t have to scramble to cover bills.

2) Helps Protect Illiquid Assets

Some of the most valuable assets—homes, family property, or a business—aren’t easy to sell quickly. Insurance proceeds can reduce the pressure to sell assets fast or below value just to cover costs.

3) Can Make Inheritances More Equitable

Not every asset splits neatly. If one beneficiary receives a business or property, life insurance can help balance value for other heirs in a way that feels fair and reduces conflict.

4) Supports Loved Ones Through Transition

Even when an estate plan is clear, there can be a financial “gap” after someone passes away—income stops, bills continue, and timelines stretch. Insurance can help provide stability while everything else is being sorted out.